2/17/2015 1:39:00 AM

HEADLINES

USITC: Chinese Wire Rod Imports Gained 11.7% of Market

![]()

MARKET SUMMARY

The leading U.S. producers of wire rod are Charter, Gerdau, Keystone, Nucor, and Sterling Steel Company LLC (“Sterling”), while leading producers of wire rod in China include Benxi Beiying Iron and Steel Group Co., Ltd., Hebei Iron and Steel Group Co., Ltd., Jiangsu Shagang Group Co., Ltd., Qiananshi Jiujiang Wire Co., Ltd., Wuhan Iron & Steel Group Corp., and Xingtai Iron & Steel Co., Ltd.

Apparent U.S. consumption of wire rod totaled approximately 5.3 million short tons ($3.8 billion) in 2013. U.S. producers’ U.S. shipments of wire rod totaled 3.6 million short tons ($2.5 billion) in 2013, and accounted for 67.8% of apparent U.S. consumption by quantity and 67.3% by value.

U.S. imports from China totaled 618,790 short tons ($335.9 million) in 2013 and accounted for 11.7% of apparent U.S. consumption by quantity and 8.9% by value. U.S. imports from nonsubject sources totaled 1.1 million short tons ($895.7 million) in 2013 and accounted for 20.5% of apparent U.S. consumption by quantity and 23.8% by value.

The U.S. International Trade Commission issued detailed findings of its investigation (Investigation Nos. 701-TA-512 and 731-TA-1248 (Final), USITC Publication 4509, December 2014) that culminated with the December 2014 unanimous vote to apply anti-dumping and countervailing duty orders on imports of carbon and certain alloy steel wire rod from China. (Click here for duty rate graph.)

{kind=link}

Apparent U.S. consumption of wire rod increased from 5.13 million short tons in 2011 to 5.33 million short tons in 2012, then declined to 5.31 million short tons in 2013, for an overall 2011-13 increase of 3.5%, according to the Commission’s public report ‘Carbon and Certain Alloy Steel Wire Rod from China’ (Investigation Nos. 701-TA-512 and 731-TA-1248 (Final), USITC Publication 4509, December 2014).

The domestic wire rod industry’s share of apparent U.S. consumption declined from 75.6% in 2011 to 67.8% in 2013.

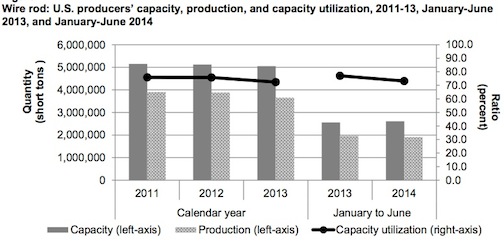

The capacity of the ten U.S. wire rod producers rose by 1.9% between 2011 and 2013, but “remained at a level near that of apparent U.S. consumption throughout the period of investigation,” the report found.

Most U.S. producers reported that they are not operating at full capacity due to market conditions, and that import competition limits their ability to produce more wire rod. A number of U.S. producers reported production curtailments, although a few domestic producers have expanded or made improvements to their production facilities during the period of investigation.

Nonsubject countries are the largest suppliers to the U.S. wire rod market after the domestic industry. Their share of apparent U.S. consumption declined from 24.4% in 2011 to 20.5% in 2013. Canada was the largest individual source of imported wire rod in 2011 and 2012 and the second largest after subject imports from China in 2013.

The U.S. already has antidumping duty orders in effect on wire rod from Brazil, Indonesia, Mexico, Moldova, and Trinidad and Tobago, and a U.S. countervailing duty order is in effect on wire rod from Brazil.

By 2013, subject imports from China became the largest individual import source of supply to the U.S. market. The share of apparent U.S. consumption held by subject imports increased dramatically from a fraction of a percent in 2011 to 11.7% in 2013.

During the period of investigation, scrap prices decreased overall, while prices for natural gas and electricity increased overall.

Raw materials costs comprised domestic producers’ single largest component of cost of goods sold (“COGS”), raw materials costs per short ton declining from $504 in 2011 to $469 in 2012 and then to $436 in 2013.

Wire rod is primarily produced to order; U.S. producers reported that 97% of their 2013 U.S. commercial shipments were produced to order, while 99.6% of importers’ 2013 commercial shipments were produced to order. The lead times for domestically produced wire rod produced to order ranged from 15 to 75 days, and the lead time for subject imports ranged from 60 to 150 days.

Subject imports were virtually nonexistent at the beginning of the period of investigation, but increased dramatically, from 144 short tons in 2011 to 241,966 short tons in 2012, and then to 618,790 short tons in 2013. Subject import market share rose from less than 0.05% in 2011 to 4.5% in 2012 and 11.7% in 2013. (Click here for graph.)

{kind=link}

“The increase in subject import market penetration came largely at the expense of the domestic industry,” the USITC found. “The domestic industry lost 7.7 percentage points of market share from 2011 to 2013, with a decline from 75.6% in 2011 to 67.8% in 2013.

During its investigation, the USITC had 10 U.S. producers and 10 importers of subject wire rod from China provide usable pricing data for sales of the requested products. Pricing data reported by these firms accounted for 33.1% of U.S. producers’ domestic shipments of wire rod and 87.1% of U.S. shipments of imports from China.

The pricing data showed that subject imports undersold the domestic like product in 36 of 38 – or 94.7% – of total comparisons. The margins of underselling ranged from 4% to 15%, and the average margin of underselling was 9.2%.

“We find this underselling to be significant in the light of the importance of price in purchasing decisions. Indeed, subject imports gained market share at the expense of the domestic industry while this pervasive underselling was taking place.”

The unit value of net sales fell by $74 per short ton between 2011 and 2013, while the average unit value of raw material costs decreased by $68 per short ton.

“The predominant impact of the undersold subject imports was to cause the domestic industry to lose volume and market share rather than to decrease its prices.”

While the domestic industry lowered prices despite a 3.5% increase in consumption from 2011 to 2013, the industry’s ratio of total COGS to total net sales increased from 90% in 2011 to 91.7% in 2012 and then to 92.4% in 2013.

Over the period of investigation, virtually all trade and financial indicators for the domestic industry declined, in spite of increases in apparent U.S. consumption. The domestic industry’s capacity, which declined in each full year, fell by 1.9% from 2011 to 2013.

Production also fell in each full year, and was 6.5% lower in 2013 than in 2011.

Capacity utilization declined by 3.4 percentage points from 2011 to 2013.

The domestic industry’s U.S. shipments showed a pattern similar to that for production. “Total U.S. shipments declined during the period of investigation and were 7.1 percent lower in 2013 than in 2011. Commercial U.S. shipments followed the same annual trends.”

Inventories relative to total shipments increased steadily from 4.9% in 2011 to 7.4% in 2013.

“The financial performance of the domestic industry displayed substantial declines during the period of investigation, even as apparent U.S. consumption increased,” the USITC determined.

Domestic producers’ total net sales revenues declined each year, going from $3 billion in 2011 to $2.9 billion in 2012 and $2.6 billion in 2013. The industry’s raw materials costs also declined during this period, as did its total cost of goods sold.

“Because sales revenues declined at a somewhat higher rate than costs, the domestic industry’s operating income fell by more than half.”

The domestic industry’s ratio of operating income to net sales declined from 7% in 2011 to 5.1% in 2012 and 4.1% in 2013.

Meanwhile, the industry’s capital expenditures saw yearly increases. R&D expenses, which were much lower than capital expenditures, fluctuated from year to year and were higher in 2013 than in 2011.

“Despite increases in apparent U.S. consumption, the domestic industry’s trade and financial performance declined substantially over the period of investigation,” the USITC concluded. “We have found that the volume and market share of subject imports increased significantly over the period of investigation and that the increasing volume of low-priced subject imports significantly undersold the domestic like product and took market share from the domestic industry.”

The industry’s net sales revenues and operating performance declined accordingly. Indeed, as subject imports increased in quantity and market share from 2011 to 2013, the domestic industry’s output, employment, and financial performance all declined, leading USITC commissioners to conclude that “the significant volume of subject imports, which gained market share at the expense of the domestic industry through significant and pervasive underselling, had a significant impact on the domestic industry.”

FACTUAL HIGHLIGHTS

Petitioners included ArcelorMittal USA LLC, Chicago, IL; Charter Steel, Saukville, WI; Evraz Pueblo, Pueblo, CO; Gerdau Ameristeel US Inc., Tampa, FL; Keystone Consolidated Industries Inc., Dallas, TX; and Nucor Corporation, Charlotte, NC.

Investigations were instituted by the USITC on January 31, 2014. A hearing was held on November 12, 2014, with the USITC vote conducted on December 15, 2014.

In 2013 the U.S. had 10 wire rod producers in Arizona, Colorado, Connecticut, Florida, Illinois, Indiana, Nebraska, New Jersey, Ohio, Oklahoma, Oregon, South Carolina, Texas, and Wisconsin. The domestic industry employed 2,194 workers who produced U.S. shipments worth $2.5 billion.

The apparent U.S. consumption in 2013 was $3.8 billion, with the ratio of subject imports to apparent U.S. consumption at 8.9%. U.S. imports of wire rod in 2013 included $336 million worth of product from China and $896 million from other countries, including Canada, Japan, Brazil, Germany, the UK and Turkey.

Related Stories:

• Anixter Selling Fasteners Division for $380 Million

Share: